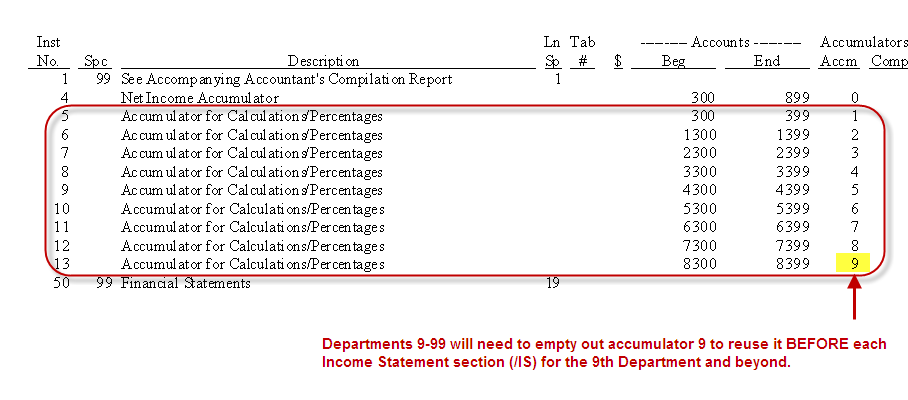

Custom Financial Statement layout for companies with 9+ departments/divisions:

- The system provides up to nine accumulators (1 to 9) for percentage comparison purposes on the Income Statement.

- These special accumulators are established in instruction numbers 5 to 14 on the financial layout.

- If a company requires more than nine accumulators these special accumulators must be reused.

- For Departmental/Divisional companies, one of the accumulators will be necessary for the Combined Account.

- There are 8 accumulators remaining after the Combined account uses accumulator 1 of the 9 available for percentage comparisons.

- Therefore, accumulator 9 must be cleared and reused for the additional departments beyond 8.

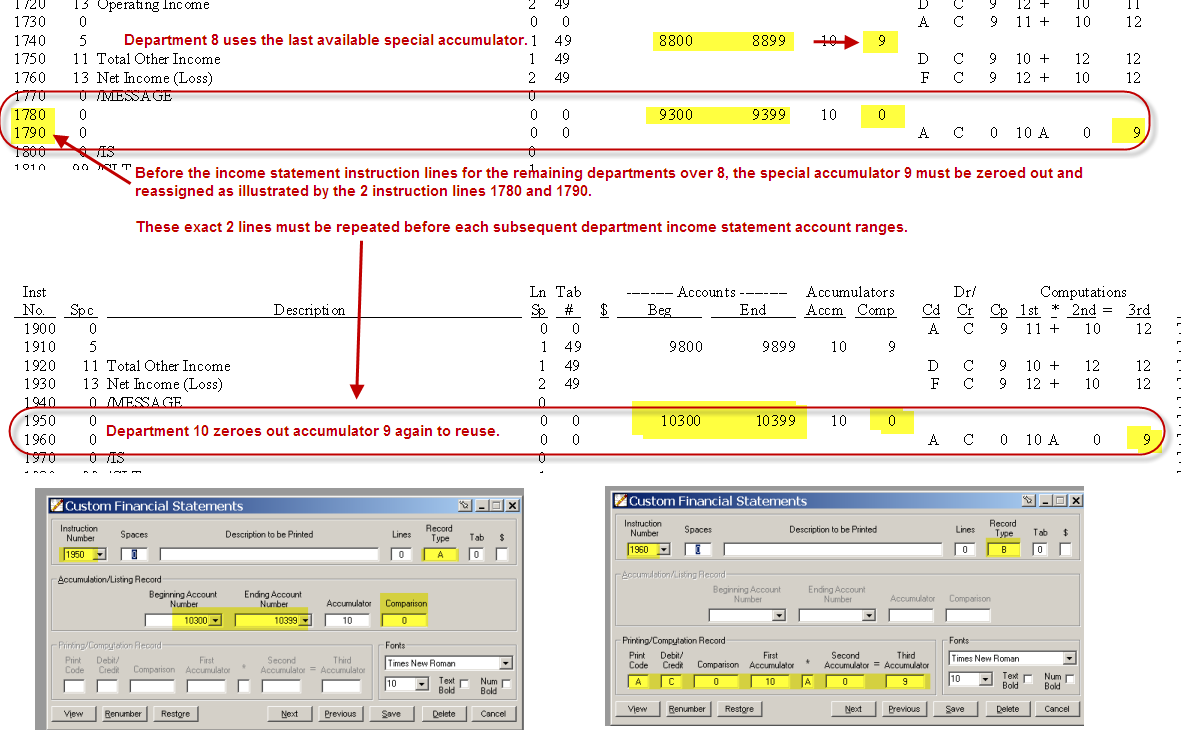

To reuse a special accumulator, clear its contents before processing the 9th and subsequent departments:

- To clear a special accumulator, place the following 2 instruction lines immediately preceding the income statement instructions section (/IS) for each additional department after 8:

- Set up a Type A record to zero out the current balance in accumulator 9 and replace it with the total sales from the next department, as indicated by the beginning and ending account ranges for the next department. (See instruction 1780 in the illustration that follows)

- Set up a Type B record to add the afore mentioned accumulated sales amount to the absolute number 0 and place the result in accumulator 9. (See instruction 1790 in the illustration that follows)

- The amount previously stored in 9 is replaced by the new amount.

- Accumulator 9 is then used to compare with the following department?s (department 9 -99) expense accounts.

You are now ready to process more than eight departments. For further reading go to the Help menu in EasyACCT, select Manuals > Reports, Chapter 3 Designing Financial Statements.